“How much will my Medicare coverage cost me out of pocket?”

This is a common question for adults age 65 and older—or those approaching Medicare eligibility. For many older Americans, especially individuals living on a fixed or limited income, Medicare expenses are a critical financial consideration. Understanding out-of-pocket (OOP) costs is the first step toward making informed decisions about your health care coverage.

“Medicare out-of-pocket expenses often change from year to year, just as your health care needs do,” explains Ryan Ramsey, Associate Director of Health Coverage and Benefits at NCOA. “When you understand these costs, you’re better prepared to plan your health care priorities, manage your finances, and reduce the risk of unexpected medical bills.”

What Does ‘Out-of-Pocket’ Mean in Medicare?

Out-of-pocket costs are the expenses you are responsible for paying after Medicare pays its portion of your health care bill. These costs vary based on the type of Medicare coverage you choose, the providers you use, and the services you receive. Some expenses—such as Medicare Part B premiums—may also depend on your annual income.

What Are Typical Medicare Out-of-Pocket Costs?

Below is an overview of common out-of-pocket expenses associated with different Medicare coverage options. Actual costs may vary depending on your plan details and health care usage.

Medicare Part A (Hospital Insurance)

Most people qualify for premium-free Part A after working at least 10 years and paying Medicare taxes. If you do not qualify, monthly premiums can be as high as $565. In 2026, inpatient hospital stays require a $1,736 deductible per benefit period.

Medicare Part B (Medical Insurance)

The standard monthly Part B premium for 2026 is $202.90, which applies to most beneficiaries. The annual deductible is $283, and after meeting this amount, you typically pay 20% coinsurance for Medicare-approved services—often one of the largest contributors to out-of-pocket spending.

Medicare Advantage (Part C)

Medicare Advantage plans include all Original Medicare benefits and often provide additional coverage such as dental, vision, and hearing care. The average monthly premium in 2026 is projected to drop to $14.00, down from $16.40 in 2025. These plans usually use fixed copayments instead of percentage-based coinsurance.

Medicare Part D (Prescription Drug Coverage)

Premiums vary by plan. For 2026, the average monthly premium is estimated at $34.50 for stand-alone Part D plans and $11.50 for Medicare Advantage plans with drug coverage. Deductibles can be up to $615 annually, and the annual out-of-pocket limit for prescription drugs will increase to $2,100. After reaching this limit, covered prescriptions cost $0 for the remainder of the year. Important Note: Individuals with incomes up to 150% of the federal poverty level (FPL) may qualify for the Low-Income Subsidy (LIS or “Extra Help”), which significantly reduces drug costs.

Medigap (Medicare Supplement Insurance)

Medigap policies help cover costs not paid by Parts A and B. Premiums vary by insurer and pricing method. Some plans include deductibles, while others do not. In 2026, high-deductible Medigap Plans F, G, and J have an annual deductible of $2,950.

How Do Medicare Deductibles Work?

A deductible is the amount you must pay for covered services before Medicare begins paying its share. Once your deductible is met, you generally pay a copayment or coinsurance, and Medicare covers the remaining cost. For example, under Part A, you must pay $1,736 for a hospital stay in 2026 before Medicare coverage applies. Some Medicare Advantage plans waive deductibles, though these plans may have higher monthly premiums.

What Is the Medicare Out-of-Pocket Maximum (MOOP)?

The maximum out-of-pocket (MOOP) limit is the yearly cap on how much you pay for covered health care services. Once you reach this limit, your plan covers 100% of approved costs for the rest of the year. The MOOP resets annually and is designed to protect beneficiaries from excessive medical expenses.

Important Note: Original Medicare (Parts A and B) does not include an out-of-pocket maximum. MOOP limits apply only to Medicare Advantage and certain Medigap plans.

2026 Out-of-Pocket Maximums

Medicare Advantage (Part C)

In 2026, the maximum allowed MOOP will decrease to $9,250, though many plans set lower limits. Prescription drug costs under Part D do not count toward this MOOP.

Medigap Plans

- Plan K MOOP: $8,000

- Plan L MOOP: $4,000 Once these limits are reached, the plan pays 100% of covered services for the remainder of the year.

Starting in 2025, all Medicare Part D and Medicare Advantage plans include a $2,000 annual cap on prescription drug out-of-pocket costs, significantly reducing expenses for beneficiaries with high medication needs.

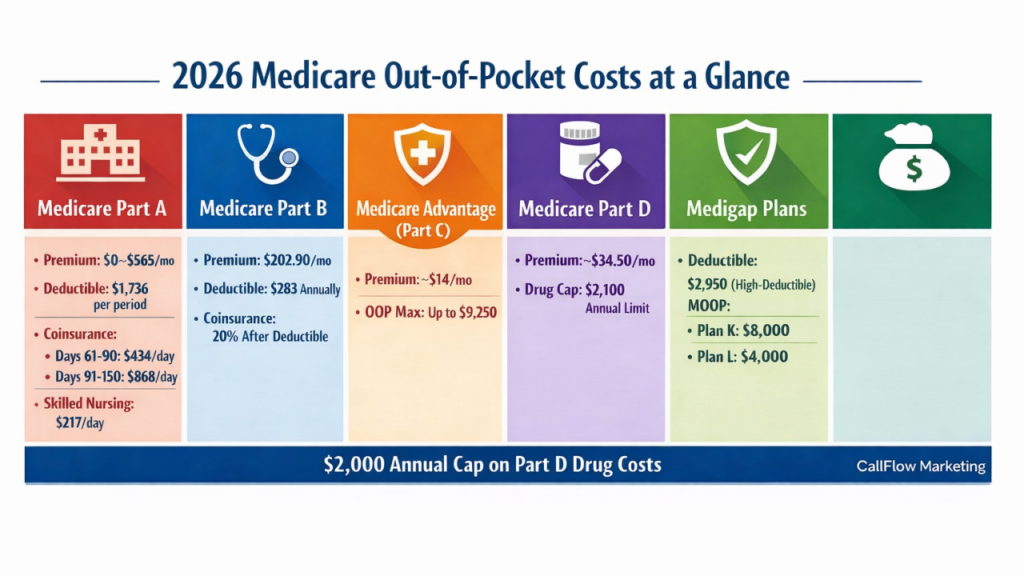

2026 Medicare Out-of-Pocket Costs at a Glance

Medicare Part A:

- Premium: $0 for most; otherwise $311 or $565/month

- Deductible: $1,736 per benefit period

- Coinsurance: Days 1–60: $0Days 61–90: $434/day Days 91–150*: $868/day

- Skilled Nursing Facility Coinsurance (Days 21–100): $217/day

- Out-of-Pocket Maximum: None

Lifetime reserve days are limited and may only be used once.

Medicare Part B:

- Premium: $202.90/month (higher for high-income earners)

- Deductible: $283 annually

- Coinsurance: 20% after deductible

- Out-of-Pocket Maximum: None

- Preventive Services: Many covered at 100%

Medicare Part C (Medicare Advantage):

- Premium: Varies; average ~$14/month

- Deductible & Coinsurance: Varies by plan

- Out-of-Pocket Maximum: Up to $9,250

Medicare Part D:

- Premium: Average ~$34.50/month (stand-alone plans)

- Deductible: Up to $615 annually

- Out-of-Pocket Drug Cap: $2,100

- Catastrophic Coverage: $0 after cap is reached

- Medigap:

- Premium: Varies

- High-Deductible Plans F, G, J: $2,950 deductible

- Out-of-Pocket Maximum Plan K: $8,000Plan L: $4,000